Financial Planning Accounts Everyone Should Have

Most people have a checking account, and maybe a savings account they rarely touch. That's a start, but it isn't a plan. Having the right accounts in place is less about how much money is sitting in them and more about building the habit and flexibility to keep growing, no matter what stage of life you're in.

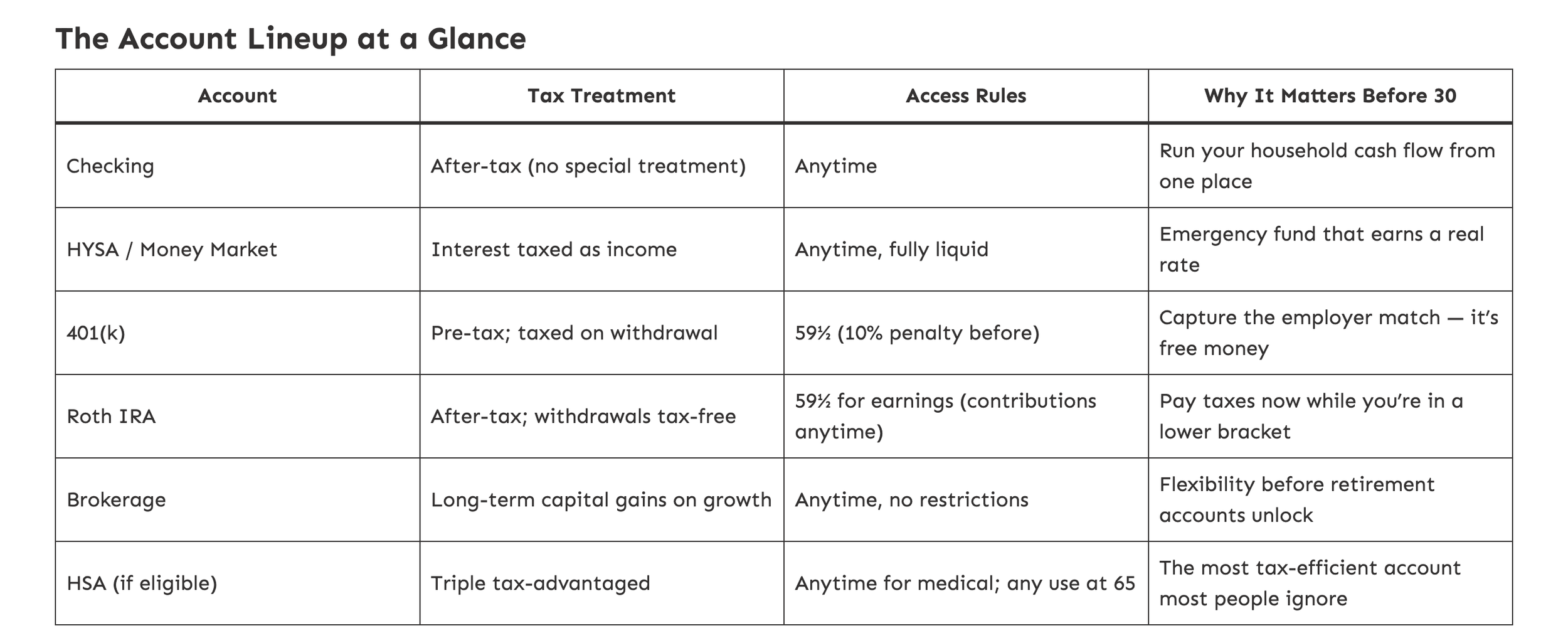

A Checking Account Worth Having

Everyone needs one, but not all checking accounts are the same. The goal is simple: income comes in, bills go out, and cash flow can be tracked from one place. What isn't necessary is paying a monthly fee for the privilege. Look for a bank with no account fees, or one where direct deposit waives them. A brick-and-mortar bank is often a better fit than an online-only service. If something goes wrong, being able to walk in and talk to a real person matters more than most people expect, until they actually need it.

A Savings Account That Actually Earns Something

Many people keep their emergency fund in a regular savings account earning close to nothing. That money should be working, even a little. A money market account or a high-yield savings account can earn meaningfully more while remaining fully liquid. No terms, no penalties, no waiting. Keeping this account separate from checking also makes its purpose clear: it isn't for spending, it's there for when life happens. A good target is three to six months of essential expenses, though even $1,000 is a meaningful starting point.

A 401k, At Least Up to the Match

If an employer offers a 401k match, contributing enough to capture it is essential. A common structure is a 4% match, meaning a 4% contribution is met with another 4% from the employer, an immediate 100% return before the money is ever invested. Pre-tax contributions also reduce taxable income in the year they're made. For those who are self-employed or don't have a 401k through work, a SEP-IRA, solo 401k, or traditional IRA can serve the same purpose.

A Roth IRA

A Roth IRA is funded with after-tax dollars. In exchange, it grows completely tax-free, and qualified withdrawals in retirement are tax-free as well. For anyone currently in a lower tax bracket than they expect to be later, that trade can work in their favor for decades. The 2026 contribution limit is $7,500 per year, though reaching the maximum isn't required to make the account worthwhile. For those above the income thresholds for direct contributions, a backdoor Roth strategy is worth discussing with a planner.

A General Brokerage Account

Unlike a 401k or Roth IRA, a brokerage account carries no special tax treatment, but it also carries none of the restrictions. No age requirement, no income limits, no contribution caps. That flexibility is the point. A brokerage account provides access to funds before retirement accounts unlock, whether that's for a major purchase, a home project, or an unexpected opportunity.

An HSA, If Eligible

For those on a high-deductible health plan, a Health Savings Account may be the most overlooked account on this list. It's the only account with triple tax advantages: contributions are pre-tax, growth is tax-deferred, and withdrawals for qualified medical expenses are tax-free. After age 65, funds can be used for any purpose, taxed similarly to a traditional IRA. Health care tends to be one of the largest expenses in retirement, and this account is built specifically to help offset it.

The First Move

Not every account needs to be funded right away. What matters is being intentional about which one comes next. For those just getting started, a good first step is making sure enough goes into a 401k to capture the full employer match, then opening a Roth IRA and contributing something, even $50, before the month ends. Getting started beats getting it perfect every time. If you'd like to talk through which accounts make sense for your situation, schedule a conversation today.